LONDON, Nov 30 (Reuters) – A $12 billion takeover proposal for Telecom Italia by private equity giant KKR has highlighted an ‘Italian discount’, which a surge in investor interest and a European fund aimed at supporting its struggling economy could help narrow.

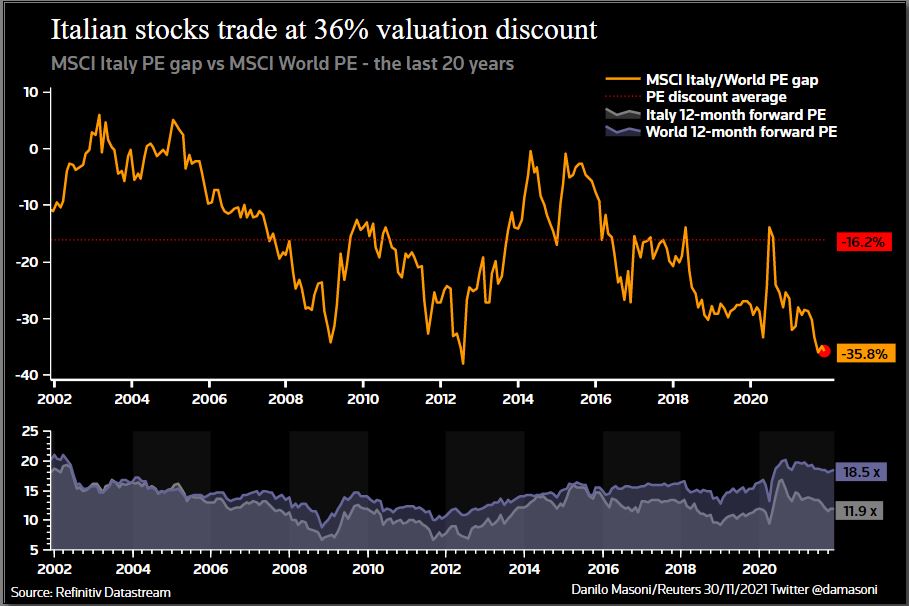

At a 36% discount to world stocks, based on 12-month forward earnings, Italian equities (.dMIIT00000PUS) trade at the widest discount in nine years and at more than twice their own 20-year average of 16%.

Meanwhile, the broader euro zone equity market (.dMIEM00000PUS) trades at a 13.8% discount to world indices and only 1.2 times the discount to its own 20-year average.

Explanations for this disparity include Italy’s index composition, which is heavy in “old economy” energy and banking stocks with nearly two-thirds of Italian blue chips (.FTMIB) made up of financial firms, utilities, telecom, oil and gas companies, while only around 20% of the 50 largest companies in the euro zone (.STOXX50E) operate in those sectors.

But above all, two decades of near-zero economic growth, an ageing population and Italy’s high debt levels have dragged down equity prices in the country.

“Italian equity markets are cheap in a global context and this has given us the opportunity to own some great companies that would trade on much higher valuations if they were to be listed in other countries like the U.S.,” said James Matthews, European equities fund manager at Invesco, citing small appliances maker De’ Longhi (DLG.MI) as an example.

Although De’ Longhi shares rose from 11 euros in March 2020 to a price of 29 euros now, after touching record high of 40 euros in September 2021, their price-to-earnings (PE) ratio of 13.5 times is lower than French competitor Seb’s (SEBF.PA) 15.6 and below the average of 17 for the STOXX 600 (.STOXX).

ITALIAN DISCOUNT

In the case of Telecom Italia (TLIT.MI), even after a 50% share price jump following KKR’s proposal it remains among the cheapest in its sector with the offer implying an enterprise value below 6 times core earnings against a sector average of 7 times, according to BofA Global Research. read more

But those who are more sceptical on Italian equities say that they can find better returns elsewhere.

“There are some good companies in Italy but on a global basis the same types of businesses in other parts of the world are more profitable and can generate higher returns on capital,” Peter Rutter, head of equities at Royal London Asset Management, said.

Even though Telecom Italia has a higher operating profit margin than rivals Telefonica (TEF.MC) and BT Group (BT.L), it has a lower return on equity, according to Refinitiv data.

Meanwhile, investors have started to take a shine to Italy’s mid-cap segment with the FTSE Italia Star index (.FTSTAR), an index of 75 small and mid-sized companies, soaring 165% since the start of the pandemic to a record high in November.

Alberto Chiandetti, a portfolio manager at Fidelity International has increased allocations to Italy, arguing such a hefty price discount is not justified for many companies as Italy stands to be the biggest beneficiary of the European Union’s 750 billion euro recovery fund. read more

An iShares MSCI Italy ETF has around 18.7 million shares outstanding, up almost 180% from November last year, far outstripping inflows into an MSCI euro zone ETF , while UBS is advising higher allocations to Italy and Amundi said it is selectively repositioning in Milan-listed stocks.

As Italy plans to use some of the EU cash to upgrade its internet infrastructure, technology enabling companies have been obvious beneficiaries with shares of technology service company Reply (REY.MI) climbing 300% since the beginning of the pandemic to reach a market capitalisation of 6.3 billion euros.

“If you think about where the discount is today, I don’t think it is in small caps anymore. The discount today is more in mid, big caps or in single stock names that are still maybe undiscovered,” Chiandetti said.

")

")